Bond Market Reset: Long Yields Surge, Investors Pivot to Short-Dated Debt

As hopes for aggressive Fed rate cuts fade, long-term Treasuries sell off sharply. Investors shift toward short-dated securities amid policy uncertainty and growing fiscal concerns.

AVANTAS RESEARCH

6/18/20253 min read

The U.S. bond market is undergoing a dramatic repricing. After months of anticipation for multiple rate cuts in 2024, investors are now waking up to a new reality: the Federal Reserve may not be as dovish as once hoped. Long-dated Treasury yields have surged, with the 10-year and 30-year benchmarks climbing steadily in recent weeks. This move reflects not only sticky inflation but also heightened fiscal concerns and a more cautious Federal Reserve.

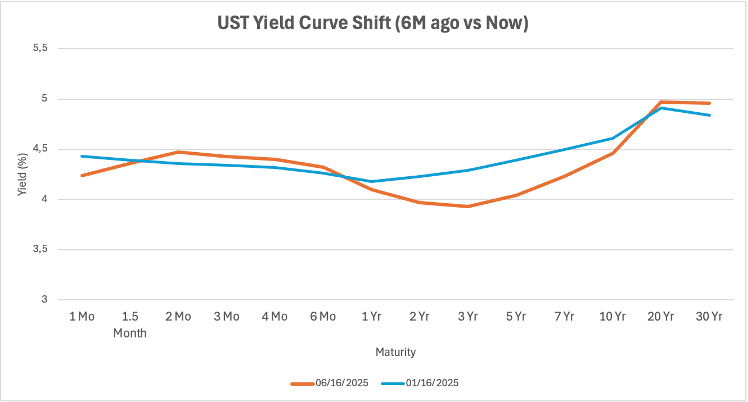

As shown by the above chart, the U.S. yield curve has steepened significantly on the long end over the past six months, with the 10Y and 30Y yields climbing while short-term rates remain anchored. This shift reflects market reluctance to hold long-dated bonds amid persistent inflation and fiscal supply pressure.

Fading Rate Cut Hopes Reshape the Curve

In early 2024, markets priced in as many as six rate cuts from the Fed. That narrative has now unraveled. Persistent inflationary pressure in services and shelter, coupled with a resilient labor market, has forced policymakers to push back against easing expectations. The Fed’s dot plot and recent public commentary from Chair Jerome Powell and other FOMC members suggest a slower path toward normalization.

This hawkish pivot is rippling across the yield curve. The 10-year Treasury yield recently climbed above 4.4%, up from below 4.1% just weeks prior. Meanwhile, short-term rates remain anchored, keeping the curve inverted but now with more pronounced upward pressure on the long end, a dynamic some analysts view as a warning signal for asset valuations

Rotation Toward Short Duration

Faced with both policy and duration risk, investors are flocking to short-dated securities. Treasury bills, money market funds, and short-term bond ETFs are seeing inflows as institutions seek safety and attractive real yields with limited price volatility.

The attractiveness is hard to miss: 3- to 6-month T-bills are yielding near or above 5.2%, offering a risk-free return that is hard to beat in a market pricing in policy inertia. Unlike longer bonds, these instruments are less exposed to market repricing should the Fed continue to hold rates higher for longer.

For portfolio managers, the risk-reward skew is clear, taking on duration in this environment means betting on a sudden Fed pivot or recession, both of which are becoming less probable in the near term.

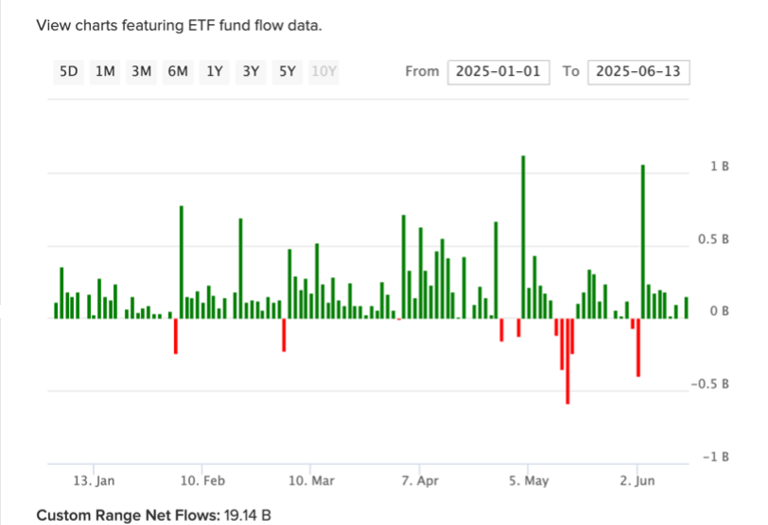

Surging Demand for Short-Term Treasuries: SGOV Fund Flows YTD

The chart highlights strong and persistent inflows into the iShares 0–3 Month Treasury Bond ETF (SGOV) from January to June 2025.

Disconnect Between Bonds, Equities, and Credit

Interestingly, while bond markets are flashing red, equity markets continue to rally. The S&P 500 hovers near all-time highs, fueled by tech momentum and AI optimism. Credit spreads remain tight, showing little sign of stress in corporate bond markets.

This divergence raises concerns. Either bond markets are too pessimistic, or equity and credit markets are underpricing risk. With financial conditions tightening from the long-end yield surge, the burden is now on corporate earnings and economic resilience to justify current equity valuations

Investor Sentiment Turns Cautious

Survey data reflects a notable shift in investor positioning. According to recent fund manager reports, cash allocations are rising, and duration exposure is at multi-year lows. While outright panic is absent, the prevailing tone is one of cautious repositioning, risk-off in duration, selective in equities, and overweight in cash.

Some asset managers are also eyeing real assets and inflation-linked bonds as hedges, though flows into those instruments remain modest compared to the pivot into short-term paper.

What to Watch: Data, Deficits, and Dissonance

Looking ahead, market participants will be watching key economic data, especially inflation and employment, as well as fiscal developments. The U.S. Treasury’s rising issuance needs and expanding deficit are placing additional pressure on the long end of the curve.

If inflation cools materially or recession signals emerge, the bond market may reverse course. Until then, the message is clear: don’t fight the Fed, and don’t fight duration risk.

Key Highlights

• FOMC Meeting (June 20): Expected to hold rates at 5.50%

• Fed Chair Powell Press Conference (June 21): High market impact expected

• US GDP (Q4 Final) (June 23): Forecast at 3.2%

• BOJ Policy Meeting (June 25): Expected to hold at -0.10%

• US PCE Price Index (June 26): Key inflation indicator

• Eurozone CPI (June 29): Forecast at 2.6%

Invest101.blog

Articles and resources for smart investing.

Contact

contact@invest101.blog

© 2025. All rights reserved.